Quick facts

- Australian Government Commonwealth Rent Assistance (CRA) key findings include:

- At June 2020, around 1.7 million income units (individuals or group of related persons) were receiving Commonwealth Rent Assistance (CRA).

- From June 2019 to 2020, the number of income units receiving CRA increased from 1.29 million to 1.7 million.

- 2 in 5 (29% or 487,900 income units) were considered to be in rental stress after receiving CRA.

- In 2020, 31% of those receiving CRA and JobSeeker Payment (Newstart Allowance) were in rental stress; a decrease from 60% in 2019.

- State/territory government provided programs in 2019–20:

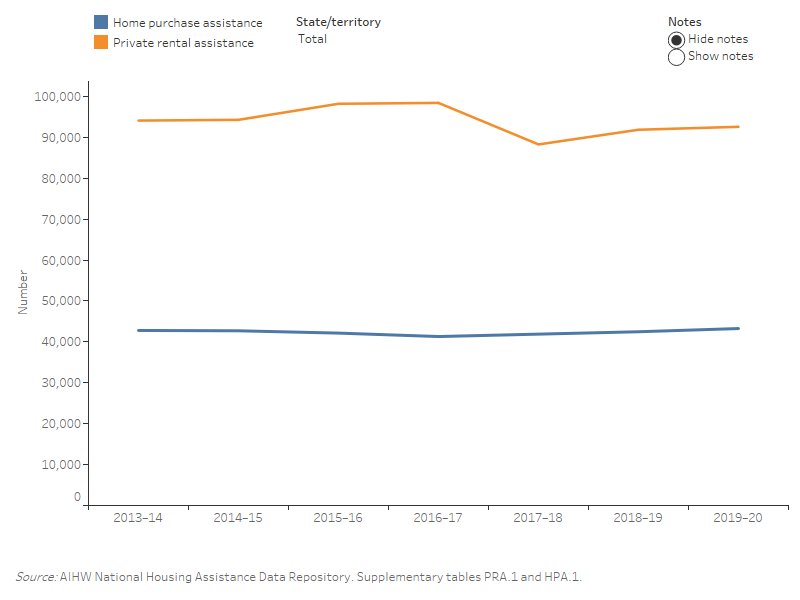

- Around 92,600 households received Private Rent Assistance (PRA).

- Home Purchase Assistance (HPA) was received by 43,300 households.

- PRA was more likely to be provided to recipients in major cities compared with HPA (63% and 58% respectively).

Financial assistance is a sizeable part of the broader provision of housing assistance in Australia. Governments provide various forms of financial support to assist people on lower incomes to meet housing costs, whether it is rental costs, mortgage repayments, saving a deposit for a home purchase or accessing finance. Housing costs are often a major expense for lower income earners and, therefore, financial assistance can be seen as an important safety net.

This section primarily focuses on the following three types of financial assistance:

- assistance with rental costs through the:

- Commonwealth Rent Assistance program

- Private Rent Assistance programs

- assistance with buying a home through Home Purchase Assistance programs.

Commonwealth Rent Assistance (CRA)

CRA is the most common form of housing assistance received by Australian households. It is an Australian Government payment to families and individuals who pay or are liable to pay private rent or community housing rent, over specified thresholds and are in receipt of:

- a social security or veterans’ income support payment; and/or

- receive Family Tax Benefit Part A at greater than the base rate.

Commonwealth Rent Assistance

CRA is a non-taxable payment, generally paid fortnightly to eligible recipients as part of a recipient’s primary payment rate. To be eligible, families or individuals paying private rent must: be in receipt of a social security or veterans’ income support payment and/or more than the base rate of Family Tax Benefit Part A, and pay or be liable to pay more than the specified rent thresholds.

CRA eligibility is based on eligibility for the primary payment and it forms part of the rate of payment. For information about CRA eligibility, see Department of Social Services.

CRA is paid at 75 cents for every dollar above a minimum rental threshold until a maximum rate (or ceiling) is reached. The minimum threshold and maximum rates vary according to the household or family situation, including the number of children.

Certain social housing tenants are eligible for CRA, such as those living in community housing or Indigenous community housing and, in some states and territories, state owned and managed Indigenous housing (SOMIH). CRA is not generally payable to public housing tenants as state and territory housing authorities already subsidise rent for these tenants.

Payment of CRA continues as long as recipients meet qualification and payability criteria for their primary payments, as well as CRA eligibility conditions.

Source: DSS 2019.

At 26 June 2020, around 1.7 million income units received CRA; around 414,200 more income units than at the same time in 2019 and around 354,200 more than the former peak of 1.35 million in 2016 (Supplementary table CRA.2). The median CRA payment was $132 per fortnight, which was equivalent to 29% of median fortnightly rent ($460 per fortnight) (Supplementary table CRA.1). For more information, see Impact of Covid-19 on the receipt of government benefits.

In 2019–20, the Australian Government’s real expenditure on CRA was $4.7 billion, increasing from $4.5 billion in 2018–19 (SCRGSP 2021). At 26 June 2020, most CRA payments were provided to income units in New South Wales (538,800 income units) followed by Queensland (436,300) (Supplementary table CRA.2).

Selected CRA recipient characteristics

At 26 June 2020, the key characteristics of the income units receiving CRA were (Supplementary table CRA.2):

- 2 in 5 (41%) were single with no dependent children

- 1 in 5 were those aged 30–39 years (22%)

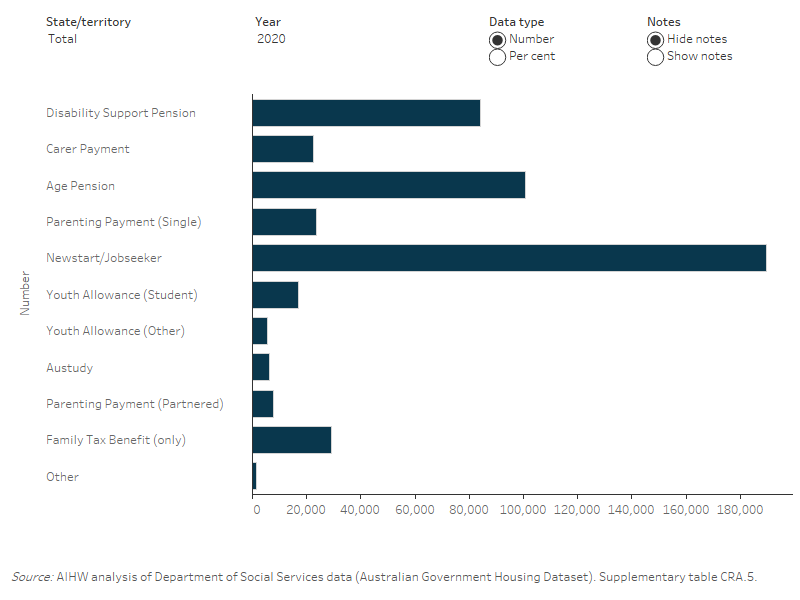

- around 2 in 5 (38%) received JobSeeker Payment followed by Age Pension (18%) as their primary payment type.

Changes over time

From 28 June 2019 to 26 June 2020, the notable changes to the characteristics of income units receiving CRA changed included (Supplementary table CRA.2):

- An increase in those also receiving JobSeeker Payment increased from 262,000 (or 20% of all CRA recipients) in 2019 to 644,300 (38%) in 2020; by contrast, there was decrease in the number receiving Family Tax Benefit (only) from 178,600 (14%) to 143,800 (9%).

- The number of Single, no children, sharer income units increased from 163,300 in 2019 to 321,900 in 2020.

For more information, see Impact of Covid-19 on the receipt of government benefits.

State and territory and selected characteristics

The profile of income units receiving CRA varied by state and territory. At 26 June 2020 (Supplementary table CRA.2):

- 2 in 5 (46%) income units in Tasmania were Single, no dependent children compared with 39% with this living arrangement in Queensland.

- Just under half (48%) of income units in the Northern Territory also received JobSeeker Payment compared with 32% in Tasmania.

- Around one in seven (15%) of income units in the Australian Capital Territory received Youth Allowance (Student); by contrast, 1.4% of income units receive this payment in the Northern Territory.

CRA entitlement

The CRA payment received as a proportion of median fortnightly rent varied by location. In Sydney, an income unit’s CRA entitlement was 24% of rent (median fortnightly rent of $550), while in the rest of New South Wales, the CRA entitlement was a greater proportion of rental costs, at 34% (median fortnightly rent of $410), at 26 June 2020 (Supplementary table CRA.1).

For Queensland, the difference between CRA entitlements as a proportion of rent was smaller when comparing the capital city and rest of state. CRA entitlement was 27% of rent in Brisbane and 29% in the rest of the state. In Tasmania CRA entitlement was 32% in Hobart and 35% in the rest of state (Supplementary table CRA.1).

Impact of COVID-19 on the receipt of government benefits

COVID-19, JobSeeker Payment and Youth Allowance

The jobless rate in Australia increased as the COVID-19 pandemic severely affected the Australian economy (Parliamentary Library 2020). In December 2019, the seasonally adjusted unemployment rate was 5.1%, which grew to 7.5% by July 2020. By December 2020, the unemployment rate had fallen to 6.6% (ABS 2021).

In response to COVID-19 and the resulting increase in the unemployment rate, Australian Government made temporary changes to social security payments. These adjustments have increased the number of people eligible for and receiving income support payments (Parliamentary Library 2020).

Following COVID-19 in the beginning of 2020, the government introduced the Coronavirus Supplement which was payable to recipients of the following income support payments: JobSeeker Payment (formerly Newstart Allowance), Youth Allowance (JobSeeker, Student and Apprentice), Parenting Payment (Partnered and Single), Sickness Allowance, Austudy payment, ABSTUDY living allowance, Widow Allowance, Partner Allowance, Farm Household Allowance, Special Benefit, and certain Department of Veterans Affairs student payments. The information below reports on how COVID-19 affected JobSeeker Payment and Youth Allowance only.

The main income support payments available for those aged 16–65 who are able to work but unable to support themselves are JobSeeker Payment and Youth Allowance (Other). Sickness Allowance and Bereavement Allowance were incorporated into JobSeeker Payment, when it was introduced on 20 March 2020 (Parliamentary Library 2020). The timing of this change coincided with the outbreak of the pandemic in Australia and the rising unemployment. For single person with no children household, the maximum payment rate for JobSeeker Payment is $570.80 per fortnight. For a partnered person household, this is $515.40 per fortnight (Services Australia 2021c).

In response to the pandemic, the Australian Government introduced additional payments to support lower income Australians, including the Coronavirus Supplement and Economic Support Payments, available to eligible income support recipients. Over time, the amount paid to recipients changed (Parliamentary Library 2021a):

- from 27 April 2020 to 24 September 2020, recipients received $550 per fortnight

- from 25 September 2020 to 31 December 2020, recipients received $250 per fortnight

- from 1 January 2021 to 31 March 2021, recipients received $150 per fortnight.

From 1 April 2021 onwards, JobSeeker Payment and Youth Allowance increased by $50 per fortnight (Services Australia 2021b).

Rental stress and CRA

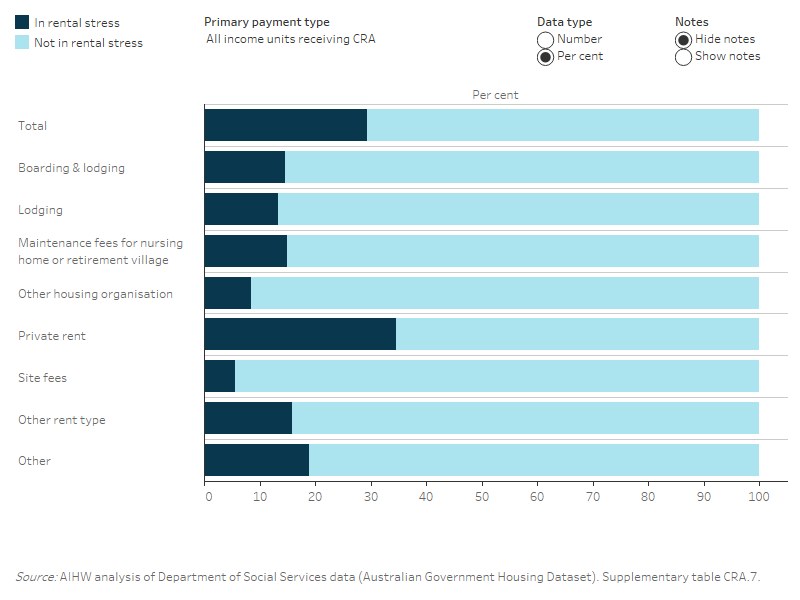

CRA has a considerable impact on reducing rental stress. Rental stress can be defined as spending more than 30% of gross household income on rent (SCRGSP 2021). At 26 June 2020, 55% of CRA recipients would have been in rental stress without CRA. With CRA this proportion was lower with 29% of CRA recipients in rental stress (Supplementary table CRA.3).

In 2020, the time-limited Coronavirus Supplement was included as income for certain types of income support payments and has been included in the calculation of rental stress.

Rental Stress, CRA and primary payment type

Rental stress for income units receiving CRA differed depending upon the primary payment type. Comparing 28 June 2019 with 26 June 2020, for income units in receipt of CRA (Supplementary table CRA.5) the proportion in rental stress after receiving CRA:

- there was a decrease from 60% to 31% for those receiving JobSeeker Payment/ Newstart Allowance

- there was a decrease from 73% to 21% among those receiving Youth Allowance (Other).

Special Needs Groups

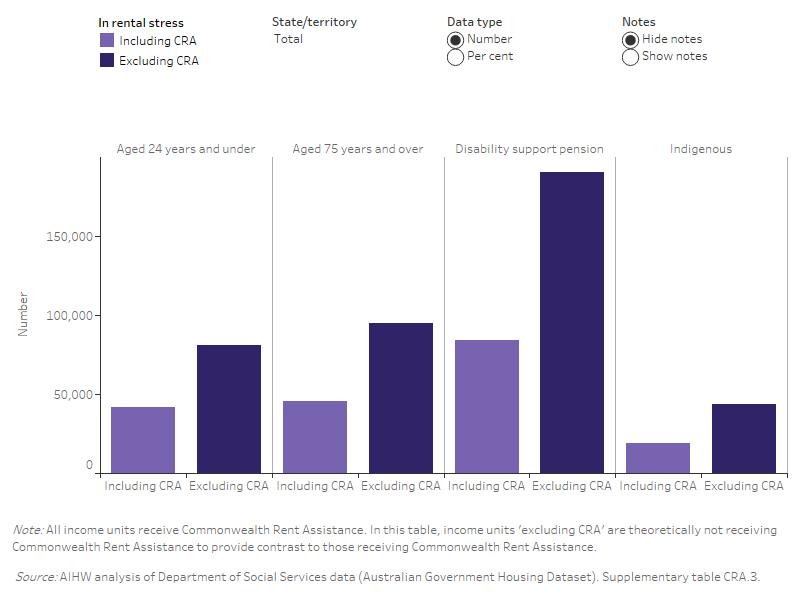

The impact of CRA on reducing rental stress varies between income unit types. At 26 June 2020, those on Disability Support Pension (32% in rental stress) were the most likely of the special needs groups to be in rental stress after CRA. (Figure FINANCIAL.1) (Supplementary table CRA.3). For income units aged 24 years and under in receipt of CRA 24% were in rental stress in 2020; by contrast, for income units aged 75 years and over the proportion in rental stress was higher at 29%. For those income units including at least one Indigenous member, around 1 in 5 (19%) were in rental stress with CRA (Figure FINANCIAL.1) (Supplementary table CRA.3).

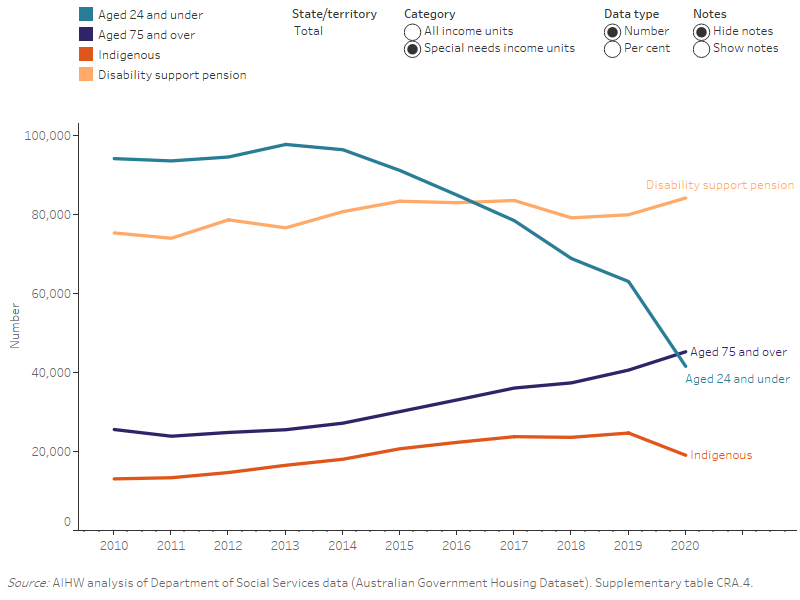

Of the income units, receiving CRA by special needs group, at 26 June 2020 (Figure FINANCIAL.1) (Supplementary table CRA.4):

- The Australian Capital Territory had the highest proportion of CRA income units aged 24 and under in rental stress (39%) followed by New South Wales (31%).

- Western Australia and the Northern Territory (34% both) had the largest proportion of income units receiving Disability Support Pension who were in rental stress; the lowest proportion were those in Tasmania (24%).