Compilation of health expenditure estimates

The HED, where the AIHW health expenditure data are collated and stored, is compiled each financial year. However, it takes approximately 15 months after the end of the reference year to receive, process, check and analyse the data, and release the HEA report.

Allocation of expenditure

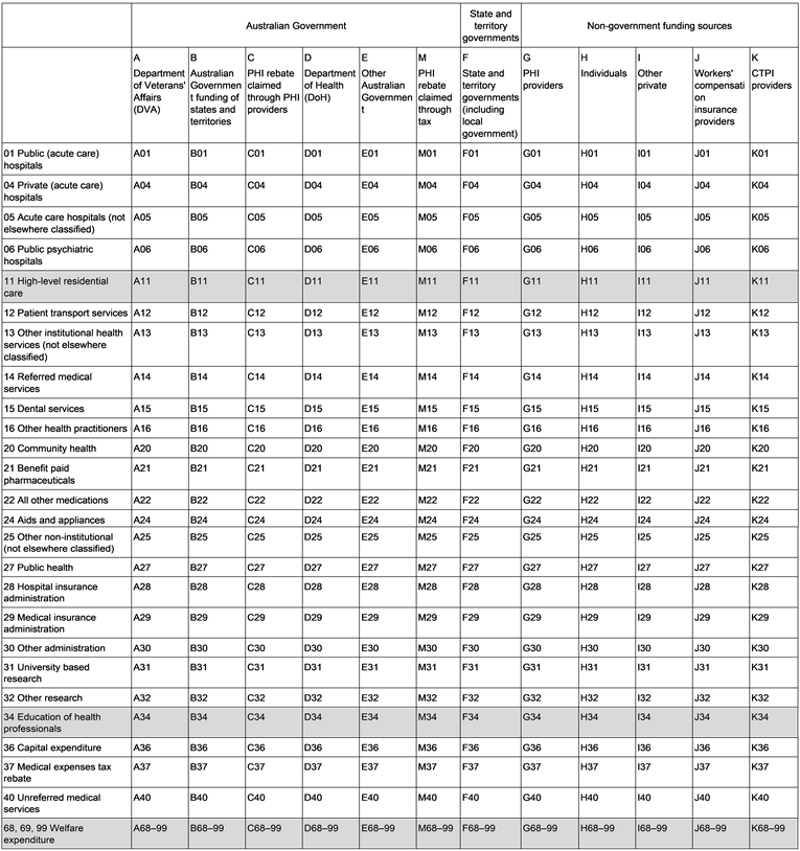

The HED is structured to reflect the flow of funds in the health system (Figure 32), each column representing a funding source and the rows, the areas of expenditure (Table T1).

Derivation of expenditure estimates are based around the source of funding approach, whereby offsets are made to avoid double counting and to reflect the original source of funding (see Offsets).

This structure is reflected further in the estimates reported in the HEA, which presents health spending firstly by source of funds and secondly by area of expenditure.

State and territory level data

Data are disaggregated and reported at the state/territory level. Where the state/territory level data are not available in the source data, the expenditure estimates are allocated to the states and territories using allocation factors such as population or medical staffing proportions.

More detailed levels of geographical and demographical data (such as Statistical Area 3, data by age group, and data by socio-economic group) are not available in the HED. Such level of details might be available in AIHW’s Disease expenditure reports.

Offsets

Offsetting is the mechanism by which an adjustment is made for potential double counting of expenditure. By applying an offset, account is taken of circumstances where the same funds are spent more than once due to the way they flow in the health system. In these instances, a decision is required about which source the expenditure will be counted against. In the ANHA the source of funds approach is used to allocate expenditure to where the funds originated. The offsets are explained in detail throughout this chapter.

An example of an offset is that, as state and territory governments receive funding from the Australian Government, such as NHR funding and health-related NPPs, the spending is counted as components of spending by the Australian Government. The corresponding amounts are then deducted from state and territory governments’ gross expenditure to remove any double counting. Revenue that state and territory governments received from other sources (such as from DVA or non-government entities) are accounted for in a similar way.

Notes:

- High-level residential care (row 11) and Education of health professionals (row 34) are not currently considered to be in the scope of health expenditure. Rows 68, 69 and 99 are set up to take welfare expenditure. Expenditure for these categories is not included in the ANHA.

Rows 01, 05 and 06 are counted as public hospital services; rows 28, 29 and 30 combine to administration; while rows 31 and 32 are counted as research.

See more : Column E - Other Australian Government

Components | Offsets | Notes |

|---|---|---|

|

|

|

Expenditure components

This column includes other spending on health by the Australian Government (except DVA, DoH, grants to states and territories and PHI rebates). The data used in estimating this are sourced from:

- Medical expenses tax offset from Treasury–Tax Benchmarks and Variations Statement. The Australian Government contributes to funding for health through the medical expenses tax rebate, available to individuals to claim through the taxation system if they have out-of-pocket medical expenses over a specified amount. As of 01 July 2019, the rebate was no longer obtainable, with a small amount of late processing in 2019–20.

- Expenditure by the Australian Government on research from ABS Research and Experimental Development statistics, generally only available every second year. The ABS research surveys used are:

- 8111.0 Research and Experimental Development, Higher Education Organisations, Australia. Tables: 81110do003 (by source of funds) and 8110do006 (by socio-economic objective). Data are available on a state/territory basis.

- 8109.0 Research and Experimental Development, Government and Private Non-profit Organisations, Australia. Tables: 81090do003 (Government expenditure) and 81090do007 (Private non-profit expenditure). Data are allocated to state/territory level using population proportions.

- Australian Government capital expenditure from ABS Government Gross Fixed Capital Formation (GFCF).

- Australian Government capital depreciation from ABS capital consumption (Economic type framework (ETF) 1231), with depreciation allocated to various areas (rows 1 to 40) using proportions calculated from DoH’s cost centre data (column D).

Spending on health research funded by the Australian Government is derived using:

- research with a health socioeconomic objective only from the ABS research surveys

- the Higher Education Organisations survey provides estimates for University based research (row 31)

- the Government and Private Non-profit Organisations survey provides estimates for Other research (row 32).

Research funded by State and territory governments and local governments is included in column F, while research funded by the private sector is included in column I (Other private).

NHMRC grants are included as other Australian Government expenditure but are offset against itself since the grants have been accounted for in the University based research from the Higher Education Organisations survey.

Capital expenditure (row 36) by the Australian Government obtained from ABS Government GFCF is available at a national level only; these estimates are allocated to states and territories based on the proportion of health and medical staff in each jurisdiction.

The ABS data on depreciation of fixed assets (ETF 1231) for the Australian Government are allocated to relevant area of spending and the state/territory level by using proportions calculated from cost centre data (processed in column D).

Since 2019–20, health expenditure by Australian Department of Defence (rows 01 to 40) has been added to the HED in column E.

Offsets

The ABS research surveys and ABS Government GFCF provide comprehensive estimates for Australian Government expenses relating to health research (rows 31, 32). Therefore, health research spending funded by DVA (column A), grants to states and territories (column B), and DoH (column D) are offset in column E to avoid double counting. Similarly, spending from DoH’s cost centres and Australian Government grants to states and territories on capital expenditure (row 36) are also offset in this column.

Notes

Medical expenses tax rebate (row 37) is treated as a subsidy by the Australian Government to Individuals. It is offset against Individuals health spending in column H.

Data processing, including data sources

The Australian Government

The Australian Government total health spending includes spending:

- by DVA (column A)

- by grants to states and territories, through NHR funding and NPPs (column B), including HSDs in public hospitals

- on PHI premium rebate claimed through providers (column C) and through taxes (column M)

- by DoH, including spending on MBS and PBS programs (column D)

- by other Australian Government agencies, such as spending on capital expenditure, capital depreciation, health research and the net medical expenses tax rebate (which had phased out by the end of 2018–19) (column E). As of 2019–20, spending by the ADF is also included.

|

Expenditure components |

Offsets |

Notes |

|---|---|---|

|

None |

|

Expenditure components

The Australian Government funds DVA by making payments through DVA for health services to eligible veterans and their dependents.

Annual expenditure statistics for estimating spending by DVA are sourced from three tables:

- ‘MRCA and SRCA’ (which are related to payments for health care under the Safety, Rehabilitation and Compensation (Defence-related Claims) Act 1988, Military Rehabilitation and Compensation Act 2004 and Safety Rehabilitation Compensation Act 1988)

- ‘Program benefits’ that qualify under DVA National Treatment Account

- RPBS.

The payments of health goods and services from ‘MRCA and SRCA’ and ‘Program benefits’ are mapped to areas of spending:

- Public hospitals (row 01)

- Private hospitals (row 04)

- Public psychiatric hospitals (row 06)

- Patient transport services (row 12)

- Dental services (row 15)

- Other health practitioners (row 16)

- Benefit paid pharmaceuticals (row 21)

- Aid and appliances (row 24)

- Other administration (row 30)

- Other research (row 32)

- Unreferred medical services (row 40).

Payments for Pharmaceutical Services in ‘Program Benefits’ is apportioned to states and territories using proportions derived from the RPBS.

DVA’s spending on Residential Nursing Home is allocated to row 11 (High-level residential care) and spending on Community Nursing is allocated to row 68 (Welfare expenditure) – these are not currently included in the ANHA.

Offsets

There are no offsets for column A.

Notes:

DVA’s spending on:

- Public hospitals are offset against State and territory governments (column F) to derive State and territory own spending on Public hospitals.

- Private hospitals are offset against Individuals (column H), which includes total patient revenue from private hospitals obtained from the PHDB.

Other research is offset against Other Australian Governments (column E) as these amounts are captured in ABS Research and Experimental Development statistics, used to estimate the total spending by the Australian Government on health research.

|

Expenditure components |

Offsets |

Notes |

|---|---|---|

|

None |

|

Expenditure components

The Australian Government contributes to funding of health services to the states and territories through the NHRA. NHR funding is primarily directed to spending on the public hospital systems managed and administered by the states and territories. Health-related payments are also made as NPPs for specific projects or outcomes.

The data used in estimating the Australian Government funding of states and territories are sourced from:

- NHR funding and NPPs from Table 36 of the Treasury Final Budget Outcome, with updates from the NHFB.

- HSDs from DoH PBS (Section 100).

These data are provided at the state/territory level.

NHR funding is assigned to Public hospitals (row 01) and Public health (row 27). Payments under NPPs are mapped to the relevant areas of spending, including:

- Public hospitals (row 01)

- Referred medical services (row 14)

- Dental services (row 15)

- Community health (row 20)

- Public health (row 27)

- Other administration (row 30)

- Research (row 32)

- Capital expenditure (row 36)

- Unreferred medical services (row 40).

Since 2019–20, the NHR funding has been including the Australian Government contribution in the National Partnership on COVID-19 Response (NPCR). Data for the NPCR entitlements are obtained from the NHFB and are allocated to public hospitals (row 01), private hospitals (row 04), community health (row 20), public health (row 27), patient transports (row 12), and capital expenditure (row 36). Personal protective equipment (subject to 2018–19 baseline) spending is allocated to rows 01, 04, 12, 20, and 27 using state and territory’s reported gross expenditure spending on those areas.

Offsets

There are no offsets for column B.

Notes

To derive state and territory own expenditure, the Australian Government funding of states and territories is offset against State and territory governments’ gross expenditure (column F) in relevant areas of spending, except for capital expenditure. The payments for HSDs in Tasmania are not offset in this manner as Tasmania does not include expenditure on HSDs in GHE NMDS.

Capital expenditure and other research are offset against the relevant areas by Other Australian Government (column E), as column E already includes the total spending by the Australian Government on health research and capital expenditure.

|

Expenditure components |

Offsets |

Notes |

|---|---|---|

|

PHI premium rebate claimed through providers: data from the DoH program cost centre expenditure. Total rebate is allocated to various areas (rows 01, 04, 12, 14, 15, 16, 20, 22, 24, 28) based on PHI provider benefit payments (data from APRA) |

None |

PHI premium rebate is offset against PHI providers (column G) in relevant areas |

Expenditure components

The Australian Government subsidises the cost of PHI by paying a rebate on the premiums paid by individuals for PHI. It is regarded as an indirect subsidy of all types of health services through PHI. The rebate can be paid directly to PHI providers (column C) or through the tax system (column M) (Box 2.2).

The data used in processing PHI rebates claimed through PHI providers are sourced from the relevant DoH program cost centre expenditure. This amount is allocated to areas of expenditure based on the proportion of benefit payments in each area by PHI providers (Box 3.1), obtained from APRA data:

- Public hospitals (rows 01)

- Private hospitals (row 04)

- Patient transport services (row 12)

- Referred medical services (row 14)

- Dental services (row 15)

- Other health practitioners (row 16)

- Community health (row 20)

- All other medications (row 22)

- Aids and appliances (row 24)

- Hospital insurance Administration (row 28)

Box 3.1: Apportioning private health insurance rebates to areas of health expenditure

Rebate amounts are allocated to areas of expenditure based on the proportion of benefit payments in each area by PHI providers.

However, not all revenue collected by PHI providers is spent on health. Data from APRA are used to compute the proportion of total PHI provider revenue paid out as health benefits and spent as health administration. This proportion is applied to calculate the total rebate amount spent for health purposes. As the result, the estimate of health spending reported in HEA is an estimate of the rebate paid out as benefits. It is therefore smaller than the total rebate paid to individuals to reduce premiums.

For example, in 2018–19, data from APRA showed that 94.3% of total PHI provider revenue was spent on health (including paid out as health benefits to members and spent on administration). As the rebate is treated as a revenue source for PHI providers, only 94.3% of the total rebate is counted as health expenditure in the same year.

More detail on the processing of these data are described in Column G – PHI providers.

Offsets

There are no offsets for column C.

Notes

PHI premium rebate amounts paid by the Australian Government are offset against PHI providers (column G) in the relevant areas of spending. Column G calculates the gross health expenditure funded by PHI providers, therefore subsidies from the Australian Government (through PHI providers and through taxes) are subtracted to derive PHI providers’ own health spending.

|

Expenditure components |

Offsets |

Notes |

|---|---|---|

|

None |

|

Expenditure components

The Australian Government contributes significantly to health funding through programs and payments administered through DoH. These include:

- payments of benefits for medical services covered by MBS

- payments of benefits for pharmaceuticals under the PBS

- direct spending on health and medical services, excluding MBS benefit payments from DoH program cost centres

- departmental expenses by DoH and Services Australia administration spending for health purpose.

Program cost centres (except the cost centre for PHI rebates claimed through PHI providers, as mentioned in column C) are mapped to the relevant areas of expenditure based on the main purpose of the service. The cost centres are checked thoroughly annually with DoH to ensure new items are included and mapped accordingly. State-specific cost centres are allocated to the relevant state or territory. For cost centres that are not state-specific, factors such as population or staff number proportions are used to allocate expenditure at the state/territory level.

These cost centres are assigned to the following areas of expenditure:

- Hospitals: Public hospitals (rows 01, 05, 06), Private hospitals (row 04)

- Primary health care: Dental services (row 15), Other health practitioners (row 16), Community health (row 20), Benefit paid pharmaceuticals (row 21), All other medications (row 22), Public health (row 27) and Unreferred medical services (row 40)

- Referred medical services (row 14)

- Other services: Patient transport services (row 12), Aids and appliances (row 24), Hospital insurance administration (row 28), Medical insurance administration (row 29) and Other administration (row 30)

- Research: University based research (row 31) and Other research (row 32)

- Capital expenditure (row 36).

Payments of benefits for medical services on the MBS are used to compute the health spending for: Referred medical services (row 14); Dental services (row 15); Other health practitioners (row 16), and Unreferred medical services (row 40).

Note that, as mentioned in Referred medical services above, since 2012–13, in-hospital MBS services have been allocated to row 14 (the majority) and row 40 (a small amount of PHC provided in hospitals) due to the unavailability of identifying whether a particular MBS service is provided in a public or private hospital.

As DoH’s spending on aged care, sports and health workforce is not currently in the scope of the ANHA, a proportion of total spending is calculated to estimate the health component of the administrative and departmental expenses of DoH. This proportion is also used for the departmental expenses of Services Australia. The results are allocated to Other administration (row 30).

Offsets

There are no offsets for column D.

Notes

Spending for research (rows 31, 32) and Capital expenditure (row 36) is offset against Other Australian Government (column E).

|

Components |

Offsets |

Notes |

|

|

|

Expenditure components

This column includes other spending on health by the Australian Government (except DVA, DoH, grants to states and territories and PHI rebates). The data used in estimating this are sourced from:

- Medical expenses tax offset from Treasury–Tax Benchmarks and Variations Statement. The Australian Government contributes to funding for health through the medical expenses tax rebate, available to individuals to claim through the taxation system if they have out-of-pocket medical expenses over a specified amount. As of 01 July 2019, the rebate was no longer obtainable, with a small amount of late processing in 2019–20.

- Expenditure by the Australian Government on research from ABS Research and Experimental Development statistics, is generally only available every second year. The ABS research surveys used are:

- 8111.0 Research and Experimental Development, Higher Education Organisations, Australia. Tables: 81110do003 (by source of funds) and 8110do006 (by socio-economic objective). Data are available on a state/territory basis.

- 8109.0 Research and Experimental Development, Government and Private Non-profit Organisations, Australia. Tables: 81090do003 (Government expenditure) and 81090do007 (Private non-profit expenditure). Data are allocated to state/territory level using population proportions.

- Australian Government capital expenditure from ABS Government Gross Fixed Capital Formation (GFCF).

- Australian Government capital depreciation from ABS capital consumption (Economic type framework (ETF) 1231), with depreciation allocated to various areas (rows 1 to 40) using proportions calculated from DoH’s cost centre data (column D).

Spending on health research funded by the Australian Government is derived using:

- research with a health socioeconomic objective only from the ABS research surveys

- the Higher Education Organisations survey provides estimates for University based research (row 31)

- the Government and Private Non-profit Organisations survey provides estimates for Other research (row 32).

Research funded by State and territory governments and local governments is included in column F, while research funded by the private sector is included in column I (Other private).

NHMRC grants are included as other Australian Government expenditure but are offset against itself since the grants have been accounted for in the University based research from the Higher Education Organisations survey.

Capital expenditure (row 36) by the Australian Government obtained from ABS Government GFCF is available at a national level only; these estimates are allocated to states and territories based on the proportion of health and medical staff in each jurisdiction.

The ABS data on depreciation of fixed assets (ETF 1231) for the Australian Government are allocated to the relevant area of spending and the state/territory level by using proportions calculated from cost centre data (processed in column D).

Since 2019–20, health expenditure by Australian Department of Defence (rows 01 to 40) has been added to the HED in column E.

Offsets

The ABS research surveys and ABS Government GFCF provide comprehensive estimates for Australian Government expenses relating to health research (rows 31, 32). Therefore, health research spending funded by DVA (column A), grants to states and territories (column B), and DoH (column D) are offset in column E to avoid double counting. Similarly, spending from DoH’s cost centres and Australian Government grants to states and territories on capital expenditure (row 36) are also offset in this column.

Notes

Medical expenses tax rebate (row 37) is treated as a subsidy by the Australian Government to Individuals. It is offset against Individuals health spending in column H.

|

Components |

Offsets |

Notes |

|---|---|---|

|

None |

|

Expenditure components

The Australian Government subsidises the cost of PHI by paying a rebate on the premiums individuals pay for this insurance. It is regarded as an indirect subsidy of all types of health services through PHI. The rebate can be paid through the tax system (column M) or directly to PHI providers, which reduces premiums (column C) (Box 2.2). Where the premium rebate is claimed through tax, PHI members pay the full premium and claim the rebate at the end of the financial year.

Data for the total PHI premium rebates claimed through tax are sourced from:

- ATO Annual report.

The rebate amounts are allocated to areas of expenditure based on the proportion of benefit payments in each area by PHI providers (Box 3.1), obtained from APRA data:

- Public hospitals (rows 01)

- Private hospitals (row 04)

- Patient transport services (row 12)

- Referred medical services (row 14)

- Dental services (row 15)

- Other health practitioners (row 16)

- Community health (row 20)

- All other medications (row 22)

- Aids and appliances (row 24)

- Hospital insurance Administration (row 28)

More detail on the processing of these data are described in Column G – PHI providers.

Offsets

There are no offsets for column M.

Notes

The PHI premium rebate amounts paid by the Australian Government are offset against PHI providers (column G) in the relevant areas of spending. Column G calculates the gross health expenditure funded by PHI providers, therefore subsidies by the Australian Government (through taxes as well as through funds) are subtracted to derive PHI providers’ own health spending.

State and territory governments

|

Expenditure components |

Offsets |

Notes |

|---|---|---|

|

|

None |

Expenditure components

State and territory governments manage and administer the public hospital system as well as many other health goods and services. These goods and services are financed by a combination of their own funding (column F), as well as funds from the Australian government and non-government sources.

The major sources of data on spending on most health activities by state and territory governments are supplied through the GHE NMDS, which includes 3 main tables:

- ‘Revenue’ – all revenue received from DVA and any payments from government departments in other states or territories in relation to cross-border charging, but excluding Australian government funding such as NHR funding. This table is categorised by revenue source and organisation type.

- ‘Gross expenditure’ – wages, salaries and supplements, employer superannuation contributions, workers’ compensation premiums and payouts, purchases of goods and services and capital depreciation for all health services. This table is categorised by organisation type and function.

- ‘Depreciation’ – consumption of fixed capital for all health services. This table is categorised by organisation type and function.

Data from GHE NMDS ‘Gross expenditure’ for each state and territory are mapped with areas of expenditure based on the organisation type, and assigned to the following areas:

- Public hospitals (rows 01, 05 and 06)

- Private hospitals (row 04)

- Patient transport services (row 12)

- Dental services (row 15)

- Other health practitioners (row 16)

- Community health (row 20)

- Public health (row 27)

- Administration (row 30)

- Other research (row 32).

GHE NMDS ‘Gross expenditure’ includes capital depreciation. Prior to 2019–20, depreciation of capital data from ABS statistics were used instead of the figures from GHE NMDS ‘Depreciation’. The ABS depreciation was allocated on the basis of the depreciation proportion by organisation function from the GHE NMDS. In 2019–20, since the ABS depreciation data did not take into account the accounting standard changes related to leases (AASB, 2016), depreciation data in Table 4 GHE NMDS are used instead.

State and territory capital expenditure (row 36, data from ABS Government GFCF) and expenditure funded by state and territory governments on health research (rows 31 and 32, data from ABS Research and Experimental Development statistics) are added to complete the gross expenditure components.

Offsets

Revenue computed for each area of spending are offset against the respective gross expenditure in each area. Data for revenue in GHE NMDS ‘Gross expenditure’ are not collected by function codes, therefore revenue data are allocated across functions (areas of expenditure) based on the proportions of gross expenditure in each organisation type. This results in a distribution of revenue for each area of spending.

Revenue from the Australian Government and non-government sources are offset against state and territory spending, including:

- revenue from DVA for public hospitals (row 01): data from DVA (processed in column A)

- revenue from PHI for public hospital services (row 01) and ambulance levy (row 12): data from APRA (processed in column G)

- NHR funding for public hospitals (row 01) and public health (row 27): data from Treasury Final Budget Outcome and NHFB.

- Since 2019–20, the NHR funding on public hospitals (row 01), private hospitals (row 04), community health (row 20), public health (row 27), and patient transports (row 12). Note that capital expenditure is not reported in the GHE NMDS, the NPCR funding allocated in row 36 is not offset in column F. More details are provided in column B.

- NPPs on various areas (various rows from 01 to 40): data from Treasury Final Budget Outcome.

- HSDs (PBS Section 100) in Public hospitals: row 01 (except Tasmania, as HSD spending is not included in Tasmania’s gross expenditure reported in GHE NMDS ‘Gross expenditure’)

- revenue from workers’ compensation insurance and CTPI for public hospital services (row 01).

Notes

There are no offsets from states and territories (column F) to other expenditure sources (other columns). However, revenues from specific sources (GHE NMDS ‘Revenue’) are used to determine the health expenditure in relevant columns, such as:

- revenue from Workers’ compensation insurance is treated as column J expenditure

- revenue from CTPI is treated as column K expenditure

- revenue from Private households (Self-funded/out-of-pocket expenditure) is treated as column H expenditure

- revenue from Other private sector is treated as column I expenditure.

Non-government funding sources

The non-government total health spending includes spending:

- by PHI providers (column G)

- by Individuals (column H)

- by Other private entities (column I)

- by Workers’ compensation insurance providers (column J)

- by CTPI providers (column K)

|

Expenditure components |

Offsets |

Notes |

|---|---|---|

|

|

|

Expenditure components

PHI providers help finance certain health goods and services. Health spending by PHI providers are the gross fund benefits paid to health providers and administration spending. Expenditure estimates are equal to gross health spending minus the PHI premium rebates (claimed through PHI providers and tax; processed in columns C and M, respectively).

APRA provides input data for these estimates, on a state and territory basis, from the following:

- PHI Membership and Benefits

- PHI Prosthesis Report

- Operations of Private Health Insurers Annual Report data.

Gross health spending by the PHI providers is mapped to the following areas of expenditure:

- Public hospitals (row 01)

- Private hospitals (row 04)

- Patient transport services (row 12)

- Referred medical services (row 14) (as discussed in Referred medical services and column D above, this is related to in-hospital MBS services where PHI shares the gap payment after the Australian Government benefit is paid)

- Dental services (row 15)

- Other health practitioners (row 16)

- Community health (row 20)

- All other medications (row 22)

- Aids and appliances (row 24)

The ambulance levy for NSW and ACT are assigned as Patient transport services (row 12). Because many NSW residents in areas close to the ACT can use the hospital services in ACT, the levy amount provided by APRA in ‘State levies’ is adjusted proportionally using ambulance levy figures from NSW Treasury and ACT Treasury.

Total administrative expenses are assigned to Hospital insurance administration (row 28).

Offsets

The Australian Government rebates for PHI premiums claimed through PHI providers and tax (columns C and M, respectively) are treated as subsidies to PHI providers, therefore these are deducted from gross expenditure by PHI providers.

Notes

The PHI provider gross health expenditure (including all subsidies) in rows 04, 14, 15, 16, 22, 24 is offset against Individuals (column H).

The spending amounts on Public hospitals (row 01) and Ambulance levy (row 12, for NSW and ACT) are offset against the relevant state and territory governments (column F).

|

Expenditure components |

Offsets |

Notes |

|---|---|---|

|

|

None |

Expenditure components

Individuals fund health goods and services through out-of-pocket costs. This includes co-payment for government-subsidised goods and services, co-payment for the cost of health goods and services with third party payers and meeting the full cost of goods and services (see subsection 2.2.2).

The data used in estimating these costs are sourced from:

- Private hospital patient revenue (row 04) from PHDB and ABS PHEC.

- Out-of-pocket contributions for health services for Referred medical services (row 14, including in-hospital and out-of-hospital MBS), Dental services (row 15), Other health practitioners (row 16) and Medical services (unreferred) (row 40) from MBS. The contribution by individuals is derived by subtracting the benefits paid from the fees charged.

- Individual contributions for medications covered by PBS Section 85 and RPBS (rows 21 and 22) from PBS and RPBS, respectively. For prescriptions that cost above the co-payment, individual contributions are assigned to Benefit-paid pharmaceuticals (row 21). For prescriptions which are priced below the co-payment, individual costs are assigned to All other medications (row 22).

- Data about payments for medications purchased in pharmacies and supermarkets (row 22) are obtained from IRI. State and territory level spending is derived using proportions obtained from historical ABS HFCE.

- Payments for prescriptions for which no benefit is payable are estimated using The Pharmacy Guild of Australia and historical data and allocated to All other medications (row 22).

- Expenditure on Dental services (row 15), Other health practitioners (row 16), Aids and appliances (row 24) is estimated using historical data and the growth rate of PHI fees charged and the growth of PHI member coverage obtained from APRA.

- revenue from individuals received by state and territory health organisations (in various rows (from 01 to 32) is from the GHE NMDS ‘Revenue’. More details on the allocation of revenue to areas of expenditure in GHE NMDS are described in the processing of column F (state and territory governments).

Offsets

- PHI gross expenditure (in rows 04, 14, 15, 16, 22, 24) (processed in column G) is offset from the total gap payment (after the government benefits) in the relevant area of spending.

- Private hospital payments (row 04) by individuals that are funded by DVA (processed in column A) are offset as DVA subsidises costs to eligible veterans and families.

- Benefit payments by injury insurance providers (rows 04, 22, 24) are offset against individual costs (processed in columns J and K), as individuals are reimbursed these costs.

- Medical expenses tax rebate (row 37), which is from Treasury–Tax Benchmarks and Variations Statement (processed in column E) to account for reimbursement of individual costs through the taxation system. This item phased out after 2018–19, though a small amount appears in 2019–20 data (late claims and processing).

Notes

There are no further notes for column H.

|

Expenditure components |

Offsets |

Notes |

|---|---|---|

|

None |

|

Expenditure components

Workers’ compensation is a form of compulsory insurance payment to employees if they are injured at work or become sick due to their work (see Workers compensation insurance providers).

Data on health expenditure by workers’ compensation insurance providers are obtained from the workers’ compensation insurance regulatory authority in each state and territory (Box 2.3) and Comcare.

Data on benefits paid by Vic, SA, ACT, NT and Comcare are mapped to the following areas of expenditure:

- Public hospitals (row 01)

- Private hospitals (row 04)

- Patient transport services (row 12)

- Referred medical services (row 14)

- Dental services (row 15)

- Other health practitioners (row 16)

- Community health (row 20)

- All other medications (row 22)

- Aids and Appliances (row 24)

- Unreferred medical services (row 40).

Data on benefits paid are not provided for several health service categories for NSW, Qld, WA and Tas. For these states, data are apportioned based on benefits paid to each area of expenditure in Vic, SA and through Comcare.

For some jurisdictions, revenues from workers’ compensation insurance providers reported in GHE NMDS ‘Revenue’ are also included in workers’ compensation insurance expenditure (in rows from 01 to 32).

Offsets

There are no offsets for column J.

Notes

The amounts funded by workers’ compensation insurance for Private hospitals (row 04), All other medication (row 22), Aids and Appliances (row 24) are offset against Individuals (column H) in the respective areas of expenditure.

The amounts of Public hospitals (row 01) funded by Workers’ compensation insurance are offset against State and territory governments (column F) for some jurisdictions.

|

Expenditure components |

Offsets |

Notes |

|---|---|---|

|

None |

|

Expenditure components

CTPI provides compensation for anyone injured or killed in a motor vehicle accident (see Compulsory third party motor vehicle insurance providers).

Data on expenditure by CTPI providers are obtained from the CTPI regulatory authority in each state and territory (Box 2.4). Each agency collects different data, with the most comprehensive information on CTPI benefits paid provided by the Transport Accident Commission (Vic) and the Motor Accident Commission (SA).

For Vic and SA, CTPI benefit expenditure are mapped with the following areas of expenditure:

- Public hospitals (row 01)

- Private hospitals (row 04)

- Patient transport services (row 12)

- Referred medical services (row 14)

- Dental services (row 15)

- Other health practitioners (row 16)

- Community health (row 20)

- All other medications (row 22)

- Aids and Appliances (row 24)

- Unreferred medical services (row 40).

The proportion of benefits paid in each area of health spending in Vic are used to allocate expenditure for each health area in NSW, Qld, WA and Tas. Population proportions are used to estimate CTPI provider health spending for ACT.

For some jurisdictions, revenues from CTPI providers reported in GHE NMDS ‘Revenue’ are also included in CTPI expenditure (in rows 01, 06, 12, 15, 20, 27, 30, 32).

Offsets

There are no offsets for column K.

Notes

The amounts funded by CTPI for Private hospitals (row 04), All other medications (row 22) and Aids and Appliances (row 24) are offset against Individuals (column H) in the respective area of expenditure.

The amounts for Public hospitals (row 01) funded by CTPI are offset against State and territory governments (column F) for some jurisdictions.

|

Expenditure components |

Offsets |

Notes |

|---|---|---|

|

None |

None |

Expenditure components

Other private expenditure is part of non-government funding of health goods and services (see Other private).

The data used for estimating spending are sourced from:

- Non-patient revenue of private hospitals (row 04) estimated from ABS PHEC and PHDB

- Capital expenditure from ABS Private GFCF (row 36)

- Expenditure funded by private non-profit organisations on health research (rows 31 and 32): data from ABS Research and Experimental Development statistics

- Revenue that state and territory health organisations received from other private sources (in various rows from 01 to 32): data from GHE NMDS ‘Revenue’.

Offsets

There are no offsets for column I.

Notes

There are no further notes for column I.

|

Data source |

Notes |

|---|---|

|

ABS Australian National Accounts: National Income, Expenditure and Product

|

These data provide information about capital expenditure (as outlined in Australian System of National Accounts (5204.0)) by:

|

|

ABS Government Finance Statistics, Australia

|

Prior to 2015, the Economic type framework 1231: depreciation of fixed assets (non-defence), which refers to amounts charged to current operations in respect of the consumption of non-current tangible assets not related to defence weapons platforms was based on the Government Finance Statistics framework outlined in 2005 (ABS Australian system of Government Finance Statistics; 5514.0). As of 2015, this category was revised to Economic type framework 1241. However, the ABS Government Finance Statistics publications and associated output continued to be published on the previous Government Finance Statistics framework as outlined in Australian System of Government Finance Statistics: Concepts Sources & Methods, Australia 2005 until September quarter 2017 (See Australian System of Government Finance Statistics: Concepts, Sources and Methods, 2015 ). |

|

ABS Australian National Accounts: National Income, Expenditure and Product

|

|

|

ABS Research and Experimental Development statistics

|

Data on expenditure and human resources devoted to research and development (R&D) carried out by higher education organisations, government and private non-profit organisations in Australia. Data classification used is based on the socio-economic objective of the research as health. Data are collected biannually. Most recent surveys:

|

|

ABS PHEC (Private Health Establishments Collection) |

The Private Health Establishments collection was an annual survey which collected information about the activities, staffing and finances of all private hospitals (private acute and psychiatric hospitals, and free-standing day hospital facilities). The results of the final survey were published in Private Hospitals, Australia, 2016–17. The ABS PHEC provided estimates of individual and other private spending on private hospitals. In 2017–18 these estimates were modelled from the final 2016–17 collection. However, as of 2018–19, individual spending was obtained from the Private Hospitals Data Bureau, while other private spending continued to be modelled on the final PHEC survey data. |

|

ADF (Australian Department of Defence) |

Unpublished data request, provided by the Joint Health Command (since 2019–20) |

|

APRA (Australian Prudential Regulation Authority) data

|

These data provide information about PHI, with most data provided on a quarterly basis at the state and territory level. |

|

ATO (Australian Taxation Office) annual report |

Data related to the PHI premium rebates claimed through tax. This information is published annually by the ATO. |

|

Comcare |

Data request, provided by Comcare |

|

CTPI data

|

Data request, provided by jurisdictions’ CTPI regulators |

|

DoH (Department of Health)

|

Data provided by DoH annually |

|

DVA (Department of Veterans’ Affairs) MRCA and SRCA |

Data request, provided by DVA |

|

DVA (Department of Veterans’ Affairs) NTA (National Treatment Account) program benefits |

Data request, provided by DVA |

|

GHE NMDS (Government Health Expenditure National Minimum Data Set)

|

The GHE NMDS collects information about the direct government and government-funded expenditure on health and health-related goods and services. The most recent NMDS was implemented from 2014. More information on the GHE NMDS can be found in AIHW METeOR. |

|

MBS (Medical Benefits Schedule) |

Data held at DoH, accessed by AIHW |

|

NHMRC (National Health and Medical Research Council) grants |

|

|

NHFB (National Health Funding Body) |

|

|

PBS (Pharmaceutical Benefits Scheme)

|

Data held at DoH, accessed by AIHW |

|

PHDB (Private Hospitals Data Bureau) |

Since 2018–19, these data were used to estimate of patient revenue in private hospitals. Prior to this ABS PHEC data provided this estimate. |

|

RPBS (Repatriation Pharmaceutical Benefits Scheme) |

|

|

The Treasury

|

Table 36 of the Treasury Final Budget Outcome provides the expenditure of the Australian Government on NHR funding and NPPs to the states and territories. This information is published annually. Net medical expenses tax rebate is included in the Tax Benchmarks and Variation Statement. |

|

Workers’ compensation data

|

|

Note: Information regarding the data sources of deflators used for analysis presented in the HEA are not included in this table (see section 2.4 and Box 2.6)